June 23, 2021 ☼ economics ☼ society

The most effective way will be for the government to enable a multi-contributor model that brings whole of society into supporting the needy.

Even before the Covid pandemic hit us, it was clear that India not only needed an effective social security system that worked for everyone, but also that it had to be reimagined for the 21st century. The gig economy is growing and like those working in the ‘informal sector’, gig workers are effectively outside the system of insurance and pensions. I shudder when I hear proposals like an urban employment guarantee scheme or universal basic income as potential solutions. These ideas fail the basic mathematics test.

As Rabindranath Tagore said, Indian society is not used to the state delivering welfare (and unsurprisingly, the state doesn’t take this task seriously). It was always society that took care of its members. According to Partha Chatterjee, Tagore held that

’before the English arrived in India, the samaj would carry out through its own initiative all the beneficial works necessary to meet people’s needs. It did not look to the state to perform those functions. Kings would go to war, or hunt, and some would even forsake all princely duties for pleasure and entertainment. But the samaj did not necessarily suffer on this account. The duties of the samaj were allocated among different persons by the samaj itself. The arrangement by which this was done was called dharma.”

Therefore, a system that accomodates this underlying, unadmitted reality is likely to do better than a cut-and-paste solution from Western country. My idea is to allow society to play an important role in helping out its needy members.

As I wrote in a Mint column

“re-imagined social security system for the 21st century must tap government, corporate and social contributions for insurance and retirement accounts. Imagine a social security account where state governments can top up the Union government’s contribution, where corporate social responsibility (CSR) funds can be applied in addition to employers’, and where charitable foundations supplement an individual’s contributions. Such a multi-contribution system is possible today.”

In the early months of the pandemic, we at Takshashila anticipated that millions of people will need support, and given the scale of the problem and the paucity of funds, we need an effective system of person-to-person cash transfers. I wrote about it in ThePrint

Imagine: you, your NGO or your company can directly contribute into the Jan Dhan account of a person you know, or an unknown person you can define based on demographic criteria (age, location, income) and get tax deductions. This socially transferred rupee will cost society far less than the 3 rupees it would, had it been administered through a government channel. It will also allow better targeting as you can better identify the needy than a faceless bureaucrat.

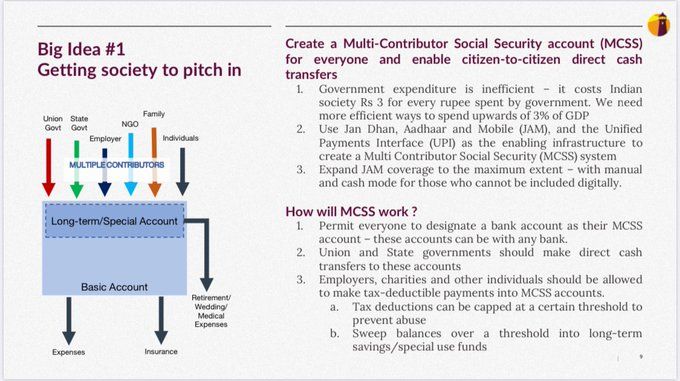

Here’s a chart that explains how this can be done.

I’ve personally seen how online crowdfunding has enabled a lot of people to help the needy. I think sites such as Milaap, GiveIndia and Ketto are pathfinders to a 21st century social security system. I’m interested in developing this further and making it happen.

© Copyright 2003-2024. Nitin Pai. All Rights Reserved.